Did you know that 90% of Americans want to be their boss? You are probably one of them. First of all, this is a great dream. Secondly, it doesn’t have to be a dream. It can become a reality.

You can either start your own business or you can buy one. Today, we will cover the second option in great detail. Are you ready to become the boss?

Starting a business with no money can be challenging, but once you seal the deal, choose one of the best website builders and create a professional website that can help you establish credibility and attract clients or investors.

Set Your New Business for Success with a Professional Website

Before we dive deep into each strategy, let’s highlight some crucial points that underscore the feasibility of no-money-down business acquisitions:

Seller financing is used in 80% of small business buys.

SBA loans can cover up to 90% of the purchase price.

Crowdfunding has opened up new ways to fund business buys.

Mixing different strategies really boosts your chances of landing a deal.

Understanding the Landscape of Business Acquisition

First things first, you need to understand the current business acquisition landscape. This knowledge will help you identify opportunities that others might miss.

The Current Market for Business Purchases

The business acquisition market is experiencing a significant shift. It’s primarily driven by demographic changes. As the Baby Boomer generation — born between 1946 and 1964 — reaches retirement age, a tsunami of businesses is hitting the market. This generation owns an estimated 2.34 million small businesses in the United States alone. Your next business venture is out there.

Interestingly, despite this flood of businesses on the market, only 30-40% of them ever successfully sell. This statistic reveals a crucial insight. Buyers have a lot of advantages and options.

Moreover, the COVID-19 pandemic has accelerated this trend. Many small business owners had to do the obvious.

Why Owners Sell: The 5 D’s and Beyond

Understanding the motivations behind business sales is crucial for potential buyers, especially those looking to structure no-money-down deals. Traditionally, business brokers have referred to the “5 D’s” as primary reasons for business sales:

Disability

Health issues that prevent owners from effectively running their business. Even established business owners will have to sell if that happens. This means you can find an income-generating business easily.

Divorce

Personal life changes that necessitate the division or sale of business assets. Many business buyers look for options like these.

Departure

Retirement or desire to pursue other opportunities. Now you can get business operations that are well-developed and even profitable.

Dissolution

Partners decided to go separate ways. This happens due to operating costs, intellectual property issues, etc.

Death

Estate sales following the passing of a business owner. Sadly, this happens. You need to identify businesses that look promising.

While these factors certainly play a significant role, they are not the only ways how you can buy a business. In fact, business owners may sell due to these reasons as well.

Burnout

The stress of running a business, especially in challenging economic times, can lead to physical and emotional exhaustion.

Technological shifts

Rapid advancements in technology may outpace an owner’s ability or willingness to adapt.

Market changes

Shifts in consumer behavior or industry trends might prompt owners to exit while their business is still valuable.

Personal goals

Desire for a career change, relocation, or simply more free time to spend with family.

Financial opportunities

Some owners may receive offers too good to refuse, even if they hadn’t initially planned to sell.

Seller financing stands out as one of the most powerful tools in the arsenal of aspiring business owners with limited capital. It’s not just a fallback option; it’s a preferred method for many transactions, offering benefits to both buyers and sellers.

What is Seller Financing?

At its core, seller financing is an arrangement where the business owner acts as the bank. It allows the buyer to make payments over time rather than providing the full purchase price upfront.

This method is remarkably common in the small business world. It is used in 80% of transactions. If you are looking for alternative financing options this might be the one. All you need is an owner financing agreement and help from your bank.

Typical Terms of Seller Financing

While terms can vary widely based on the specific circumstances of each deal, some general patterns emerge in seller financing arrangements:

Financing portion

Sellers typically finance 10-20% of the purchase price, though this can go much higher in no-money-down scenarios.

Down payment

In traditional deals, buyers often provide a down payment ranging from 30-80%, with 50% being a common benchmark. However, for no-money-down purchases, creative negotiation is key.

Interest rates

These generally fall between 6.6% and 16.5%, often slightly higher than bank rates to compensate for the increased risk.

Repayment periods

Most seller financing arrangements span 3-7 years, though longer terms are possible, especially for larger transactions.

Negotiating Seller Financing

To secure 100% seller financing—the holy grail for buyers without capital—you’ll need to get creative and offer compelling value propositions. Here are some strategies to consider:

Higher interest rates

Offering a higher interest rate can make the deal more attractive to sellers, compensating them for the increased risk.

Performance-based payments

Structure the deal so that payments increase as the business grows, aligning your success with the seller’s return.

Shorter payment terms

If possible, offer to pay off the loan more quickly than the standard 3-7 years.

Equity kickers

Offer the seller a small equity stake in the business, giving them upside potential if the company grows significantly under your leadership.

Management transition period

Propose a transition period where the seller stays involved, ensuring a smooth handover and demonstrating your commitment to the business’ success.

Future revenue sharing

Offer a percentage of future revenue for a set period, giving the seller confidence in the ongoing performance of the business.

The SBA 7(a) loan program is an appealing choice. It is made for small businesses. More precisely, those who can’t qualify for traditional bank loans. SBA 7(a) loans can cover up to 90% of the business purchase price.

The maximum loan amount is $5 million, though the average is closer to $450,000. Rates are typically based on the prime rate plus an additional percentage. Keep in mind one thing about the terms. Terms can extend up to 25 years for real estate and 10 years for other business acquisitions.

Eligibility and Application Process

To qualify for an SBA 7(a) loan, you’ll need to meet certain criteria. The business must be for-profit and operate in the United States. But, you must have invested equity (time or money) into the business. Also, other options are unavailable to you. Lastly, SBA size standards must be met.

To apply, develop a business plan, and gather all the needed documentation. Find an SBA-approved lender and apply. A special business loan is one step closer.

NoteKey details about SBA 7(a) loan program:

Loan size: from $50,000 to $5 million

Down Payment: 10% to 20%, plus a collateral

Credit requirement: A credit score of 640 or higher

Interest rate: 8% to 10.50% (accurate as of January 2025)

Loan term: up to 25 years for real estate and 10 years for anything else

Potential loan use: Buying a business or franchise, refinancing debt, working capital, or real estate purchasing

The true power of SBA loans lies in their flexibility and their ability to be combined with other financing strategies. Here are some ways to leverage SBA loans in a no-money-down acquisition:

SBA loan + Seller Financing

Use an SBA loan to cover 80-90% of the purchase price and negotiate with the seller to finance the remaining portion.

SBA loan + Equipment Financing

If the business has significant equipment assets, use an equipment loan to cover part of the down payment required for the SBA loan.

SBA loan + Investor Capital

Bring in a partner or investor to cover the down payment, using the SBA loan for the bulk of the purchase.

SBA loan + Earn-out Agreement

Structure a deal where a portion of the purchase price is paid based on future performance, reducing the initial capital needed.

3. Bring on Investors or Partners

When personal funds are scarce, turning to others with capital can bridge the gap between your entrepreneurial dreams and reality. This strategy requires strong networking skills, a compelling business case, and the ability to sell your vision to potential investors or partners.

Types of Investors to Consider

Friends and Family

Often the first port of call for budding entrepreneurs, friends, and family investors can offer more flexible terms and a higher tolerance for risk. However, it’s crucial to approach these relationships professionally to avoid personal complications.

Angel Investors

Angel investors are high-net-worth individuals who invest their own money in early-stage businesses. They often bring valuable expertise and connections along with their capital.

Venture Capitalists

Venture capitalists are typically interested in high-growth potential businesses, VCs invest pooled money from multiple sources. They usually seek larger deals and may be less suitable for traditional small business acquisitions.

Silent Partners

Individuals who provide capital without being involved in day-to-day operations. This option can be ideal for hands-on entrepreneurs who need financial backing but want to maintain control.

Strategic Partners

Companies or individuals in related industries who see value in owning a stake in your business. They might offer not just capital, but also synergies and growth opportunities.

Crafting Your Pitch

To attract investors, you’ll need a compelling pitch. Be clear about business models. If you want underperforming business be clear about that as well. You can even use a business broker. If you are asking for money upfront, specify how much. If this is no money-down deal, reveal the main elements.

Cover exit strategy as well. Even if you are looking for small business loans, this is important. You and your silent partner will know why.

Crowdfunding as an Investment Strategy

Crowdfunding has revolutionized business financing. It offers new avenues for entrepreneurs to raise capital. You can choose between equity crowdfunding and debt crowdfunding. Each one comes with pros and cons you need to know about.

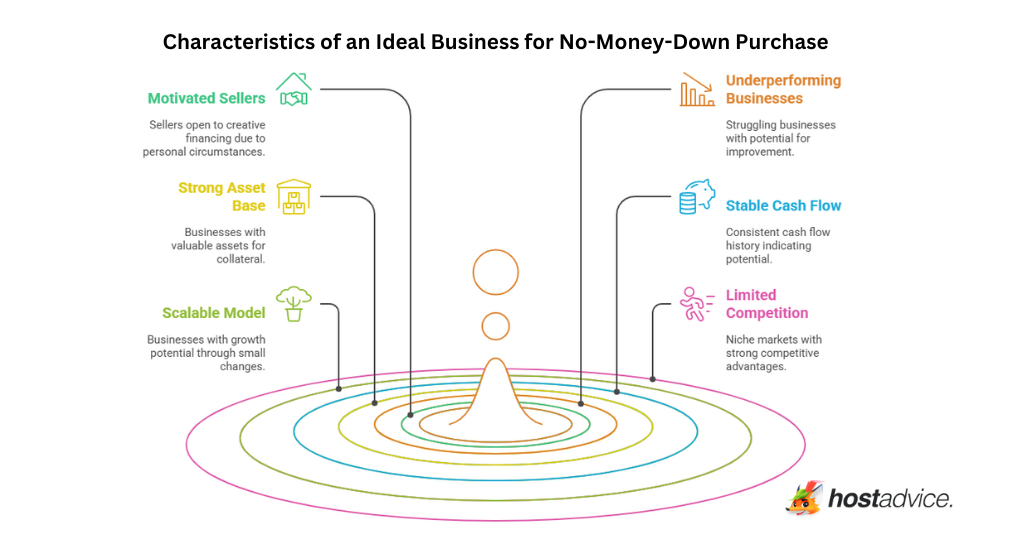

Not all businesses are created equal when it comes to no-money-down purchases. The key is to find motivated sellers and businesses with untapped potential that others might overlook.

Characteristics of an Ideal Business for No-Money-Down Purchase

Motivated Sellers

Look for businesses with owners nearing retirement, facing health issues, or those that have been on the market for an extended period. These sellers are more likely to consider creative financing options.

Underperforming Businesses

Companies that are struggling but have clear potential for improvement can be goldmines for savvy buyers. Your fresh perspective and energy could be the key to turning things around.

Strong Asset Base

Businesses with valuable assets (equipment, real estate, inventory) can provide collateral for financing, making lenders more comfortable with limited buyer investment.

Stable Cash Flow

Even if not optimal, a history of consistent cash flow can demonstrate the business’ potential and make it easier to secure financing.

Scalable Business Model

Look for businesses that can grow significantly with relatively small changes or investments.

Limited Competition

Businesses in niche market or with strong competitive advantages are often more valuable and easier to improve.

5. Offer Your Expertise in Exchange for Ownership

Sometimes, your skills and expertise can be your greatest asset in acquiring a business without money. Do you want to know how you can do this?

Structuring a Sweat Equity Deal

Identify your unique skills: Assess what specific expertise you bring to the table. This could be marketing prowess, operational efficiency, technological innovation, or industry-specific knowledge.

Find a business that needs your skills: Look for companies struggling in areas where you excel. These businesses are more likely to consider unconventional ownership arrangements.

Create a detailed proposal: Outline how your involvement will benefit the business. Include projected improvements in revenue, efficiency, or market share.

Negotiate an equity stake: Based on the value you’ll bring, negotiate for a percentage of ownership in exchange for your work.

Set clear milestones: Establish specific goals and timelines for your equity vesting. This protects both you and the current owner.

Consider a trial period: Propose a probationary period where you demonstrate your value before finalizing the equity agreement.

Draft a comprehensive agreement: Ensure all terms, including your responsibilities, equity structure, and exit strategies, are clearly documented.

Plan for the transition: If aiming for full ownership, outline a path for gradually increasing your stake as you prove your worth.

By leveraging your expertise, you can potentially acquire partial or full ownership of a business over time, turning your skills into tangible business equity.

Conclusion

By following these steps you can get your business in no time. All you need is time and a few know-hows. We have covered all the essential ones. Now it is your mission to use them and get your first business. When ready, use the same guide again and acquire another business.

If your new business doesn’t have a professional website yet, using one of these best website builders is an easy way to boost your visibility and credibility.

HostAdvice.com provides professional web hosting reviews fully independent of any other entity. Our reviews are unbiased, honest, and apply the same evaluation standards to all those reviewed.While monetary compensation is received from a few of the companies listed on this site, compensation of services and products have no influence on the direction or conclusions of our reviews. Nor does the compensation influence our rankings for certain host companies.This compensation covers account purchasing costs, testing costs and royalties paid to reviewers.